Form NR6, officially titled “Undertaking to File an Income Tax Return by a Non-Resident Receiving Rent

from Real or Immovable Property or Receiving a Timber Royalty” is a critical document for non-residents of Canada who earn rental income from Canadian real estate or receive timber royalties. By filing this form, non-residents can elect to have their rental income taxed on a net basis (after allowable expenses) instead of the standard 25% withholding on gross rental income. This option can lead to significant tax savings and better cash flow management.

Who Needs to File Form NR6?

Form NR6 is specifically designed for non-residents who:

Are Non-Residents for Tax Purposes: You do not reside in Canada and are classified as a non-resident under Canadian tax laws.

Earn Rental Income or Timber Royalties: You generate income from renting out Canadian real estate or through timber royalties from Canadian sources.

Want to Elect for Net Taxation: You wish to have your income taxed on a net basis (income minus allowable expenses) instead of the default gross withholding.

This form is particularly advantageous for individuals with substantial rental-related expenses, such as mortgage interest, property taxes, and maintenance costs, which can be deducted from gross income.

Key Benefits of Filing Form NR6

Reduced Withholding Tax: Rather than a flat 25% tax on gross income, you pay tax on your net rental income, often resulting in lower taxes.

Improved Cash Flow: Reduced withholding tax means more immediate cash available for reinvestment or personal use.

Filing Deadline for Form NR6

To take advantage of the reduced withholding tax:

You should send the CRA Form NR6 on or before January 1 of each year or before the first rental payment is due: Submit Form NR6 to the CRA before the start of the tax year (January 1) or the commencement of rental income. For example, if your rental income starts in March 2025, ensure Form NR6 is submitted by February 2025.

After the CRA approves your Form NR6, your agent can withhold non-resident tax of 25% on your net rental income (that is the amount of rental income available after the rental expenses have been paid). Your agent must pay the tax on or before the 15th day of the month after the month that the rental income is paid or credited to you.

Timely submission is crucial to avoid default gross withholding.

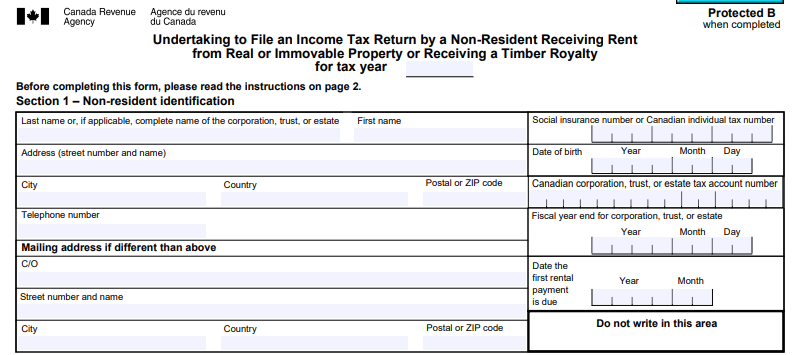

Enter your full legal name as it appears on official documents.

Provide your complete mailing address, including city, state/province, and postal/zip code.

Provide your telephone number

Input your Canadian tax identification number, such as an ITN (Individual Tax Number) or SIN (Social Insurance Number), if you have one

For corporations, trusts, and estates, provide your Canadian tax account number as well as your fiscal year end

Provide the first month of the year for which you expect to receive rental income (e.g., 2025/01)

Provide your mailing address if it is different from your residential address

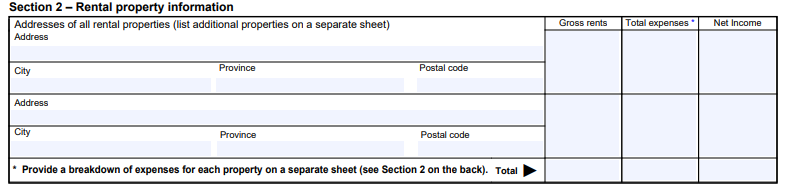

Section 2: Rental property information

List the address of each rental property or location of the timber source. If multiple properties, attach a separate sheet

Provide the estimated gross income, total expenses, and net income for the year for each property.

On a separate sheet, provide an itemized estimate of the expenses you expect to incur during the year for each property. (You have to provide this information.) Include the current and prepaid expenses that relate to the day to day management of your property. Do not include capital cost allowance, depreciation, and amortization. You can claim these amounts when you file your income tax return

Each non-resident member of a partnership filing an undertaking should report only your share of the gross rents, total expenses, and net income

Rent on real or immovable property includes crop-sharing proceeds

Section 3: Undertaking by non-resident

Sign and date the form as the non-resident taxpayer

If a representative signs on your behalf, he or she must print his or her name in the space provided and attach a copy of the power of attorney document

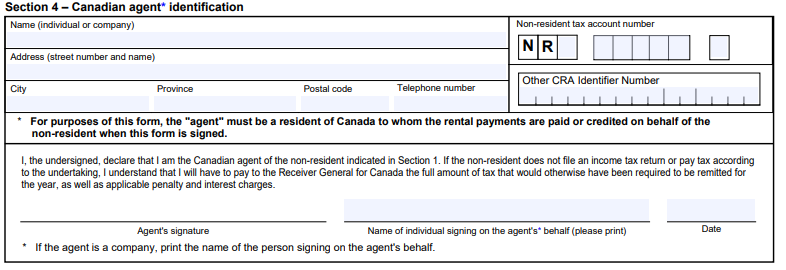

Section 4: Canadian agent identification

Provide the name of your Canadian agent (e.g., property manager)

Enter the agent’s full mailing address, including postal code and telephone number

Include the CRA withholding tax account number of the agent

The agent needs to sign and date in the designated area

Example Scenario: A Non-Resident with Two Rental Properties

Background:

John is a non-resident of Canada who owns two rental properties in Toronto:

Property 1: A downtown condo rented for $2,500/month.

Property 2: A suburban townhouse rented for $2,000/month.

Step-by-Step NR6 Filing for John:

Calculate Gross Income:

Property 1: $2,500/month x 12 months = $30,000/year.

Property 2: $2,000/month x 12 months = $24,000/year.

Gross Income ($54,000) – Expenses ($34,000) = $20,000 Net Income.

Complete Form NR6:

Section 1: John fills in his personal details and Canadian ITN.

Section 2: Both rental properties are listed with their addresses.

Gross income ($54,000), total expenses ($34,000), and net income ($20,000) are reported.

Section 3: John and his representative sign and date the form.

Section 4: John’s property manager is listed as the agent, with their address and CRA withholding tax account number.

Submit the Form:

John’s agent sends the completed Form NR6 to the CRA before January 1, 2024.

CRA Approval:

Upon approval, the agent withholds tax on the $20,000 net income instead of the $54,000 gross income, significantly reducing John’s tax burden.

Submitting Form NR6 to the CRA

You have several options to file Form NR6 with the CRA:

1. By Mail

Complete and print the form.

Mail it to the CRA’s Non-Resident Withholding Section:

Non-Resident Withholding Section

Canada Revenue Agency

PO Box 20000, STN A

Sudbury ON P3A 5C1

2. By Fax

You can also send the Form NR6 by fax at 1-866-765-8460 (in Canada and the U.S.) or 1-705-677-7712 (from anywhere else).

3. Online Submission via My Account or My Business Account

Log in to your CRA My Account (for individuals) or My Business Account (if your rental properties are part of a business).

Upload the completed Form NR6 directly to your account under the “Submit Documents” section.

4. Through a Representative

If you have authorized a tax representative (e.g., accountant or property manager), they can file Form NR6 on your behalf using their CRA Representative Account.

Obligations After Filing NR6

File an Annual Tax Return:

Submit Form T1159 (Income Tax Return for Electing Under Section 216) by June 30 of the following year.

Report actual rental income and expenses to reconcile any discrepancies with estimates.

Maintain Accurate Records:

Retain receipts and invoices for expenses.

Ensure your agent’s remittances align with CRA requirements.

Consequences of Not Filing Form NR6

Without Form NR6 approval:

Your agent must withhold 25% of gross rental income ($13,500 in John’s case).

You may need to file a tax return to claim deductions and request a refund, delaying cash flow.

Pro Tips for Success

File Early: Avoid processing delays by submitting Form NR6 well before rental income begins.

Collaborate with Experts: Work with a knowledgeable agent or tax professional familiar with CRA regulations.

Optimize Expense Deductions: Accurately estimate expenses to maximize net income benefits.

By filing Form NR6, non-residents can achieve significant tax savings, streamlined compliance, and better financial control. Whether you own a single rental property or multiple investments like John, this process ensures a more favorable taxation outcome and enhances your rental business’s profitability.

info@wiseraccounting.com

info@wiseraccounting.com

Inquire about Tax Services:

403-970-1402

Inquire about Tax Services:

403-970-1402

December 30, 2024

December 30, 2024

7 min read mins read

7 min read mins read  0 Comments

0 Comments